.png)

When planning for retirement, one of the most common questions I hear is:

“If I sell investments and realize capital gains, will those gains push me into a higher tax bracket?”

The short answer is: capital gains do not push your ordinary income into a higher bracket. But the relationship between retirement income, taxes, and capital gains is more complex than most realize.

In this guide, we’ll break down:

Watch on Youtube:

Ordinary income includes:

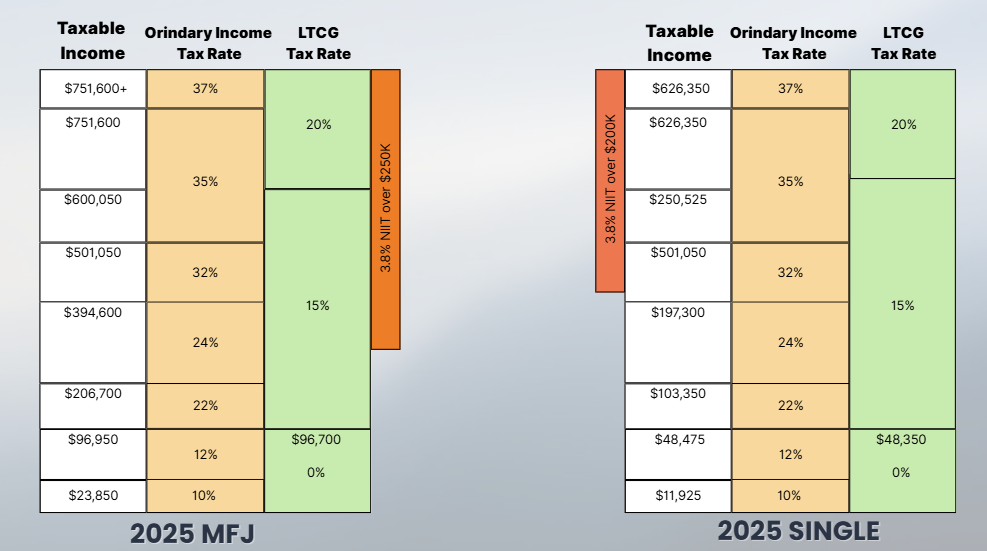

This income is taxed using a progressive system. For example, if you earn $150,000 as a married couple in 2025, you fall into the 22% bracket. But that doesn’t mean all of your income is taxed at 22%. Instead:

This “marginal” system means your effective tax rate is always lower than your highest bracket.

Capital gains are profits from selling investments held longer than one year. These are taxed more favorably than ordinary income. In 2025:

Qualified dividends fall under these same brackets.

This is why retirees often structure portfolios to maximize income in the 0% capital gains bracket.

Download the 2025 Important Numbers Worksheet (aka the "Financial Planning Cheat Sheet") here: https://www.sparkwealthadvisors.com/importantnumbers2025

Here’s the key:

That means capital gains cannot push your wages or IRA withdrawals into a higher bracket. But ordinary income can push capital gains into higher tax brackets.

There’s also the Net Investment Income Tax (NIIT)—an extra 3.8% that applies when investment income exceeds $200,000 for singles or $250,000 for married couples.

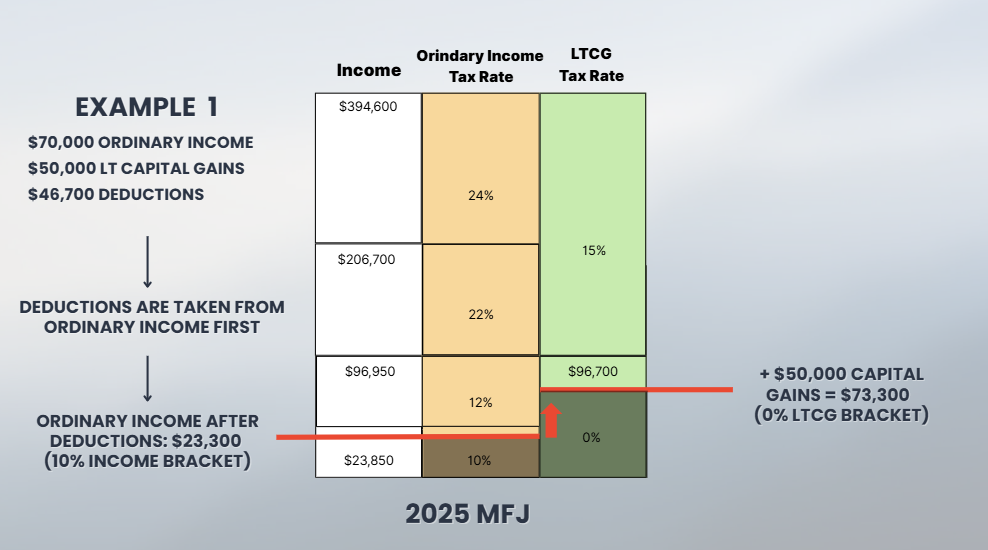

Let’s consider a married couple, both over 65:

After deductions, their taxable income is $73,300. Here’s how it breaks down:

Result: All $50,000 of capital gains fall within the 0% bracket.

👉 Conclusion: They pay no capital gains taxes. Their ordinary income also remains safely in the 10% bracket.

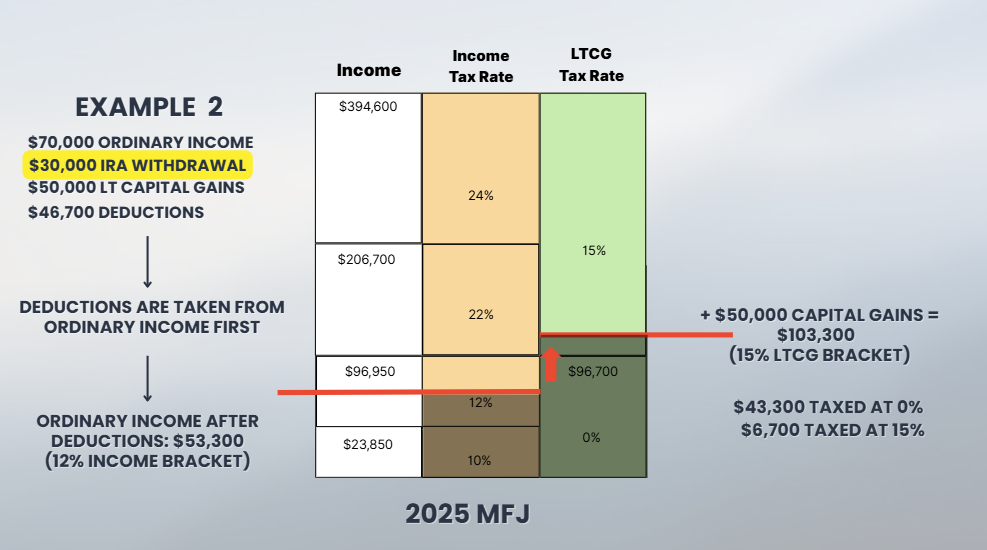

Now, let’s assume the same couple also withdraws $30,000 from a traditional IRA.

After deductions, taxable income is $103,300.

Here’s what happens:

Conclusion: The IRA withdrawal didn’t change their wages’ tax bracket, but it caused some of their capital gains to be taxed at 15%.

What if the couple withdrew an extra $1,000 from their IRA?

At first glance, you’d think they’d just owe 12% ($120). But here’s what really happens:

The effective cost of that $1,000 withdrawal? Roughly 30% in taxes.

Conclusion: In retirement, even a small increase in ordinary income can have outsized tax effects due to interactions with deductions and capital gains.

Your Social Security is taxed based on provisional income:

Capital gains add to AGI, which can trigger more of your Social Security being taxed.

Medicare premiums increase at higher Modified Adjusted Gross Income (MAGI) levels. Since capital gains increase AGI, they may also cause you to cross IRMAA thresholds.

As we saw, the new senior bonus deduction phases out at higher income levels. Capital gains can indirectly reduce tax breaks you might otherwise rely on.

Taxes in retirement are more than just brackets—they’re about coordination between income sources, investment sales, and government benefits.

That’s why smart retirees focus on retirement tax planning strategies, such as:

If you’re unsure how to put these rules into practice, consider working with a fiduciary financial planner. The right planning can reduce lifetime taxes and give you more control over your retirement income.

Capital gains may not push your ordinary income into a higher bracket, but ordinary income absolutely can push your capital gains into a higher rate. The interplay between the two systems is one of the most overlooked parts of retirement tax planning.

Understanding these mechanics—and planning accordingly—can mean the difference between paying 0% and paying 15% (or more) on your investment income.