Beyond Index Funds: A Practical Guide to Factor Investing

Index funds have transformed investing for the better: broad diversification, low costs, and a disciplined, evidence-based way to capture market returns. But just as nutrition science evolved beyond the old food pyramid, investment research has uncovered ways to build on that solid foundation. Factor investing does exactly that—maintaining diversification and low costs while tilting a portfolio toward characteristics that have historically produced higher expected returns.

This guide explains what factor investing is, why the evidence supports it, and how to integrate it thoughtfully into retirement, taxes, and planning decisions.

What Factor Investing Is (And Isn’t)

Factor investing keeps the indexing DNA: rules-based, diversified, and cost-conscious. The difference is the weighting. Traditional market-cap indexes allocate more to the largest companies, which means you automatically own more of what has recently gone up in price. Factor strategies deliberately tilt toward traits with long-term evidence of higher expected returns while staying broadly diversified.

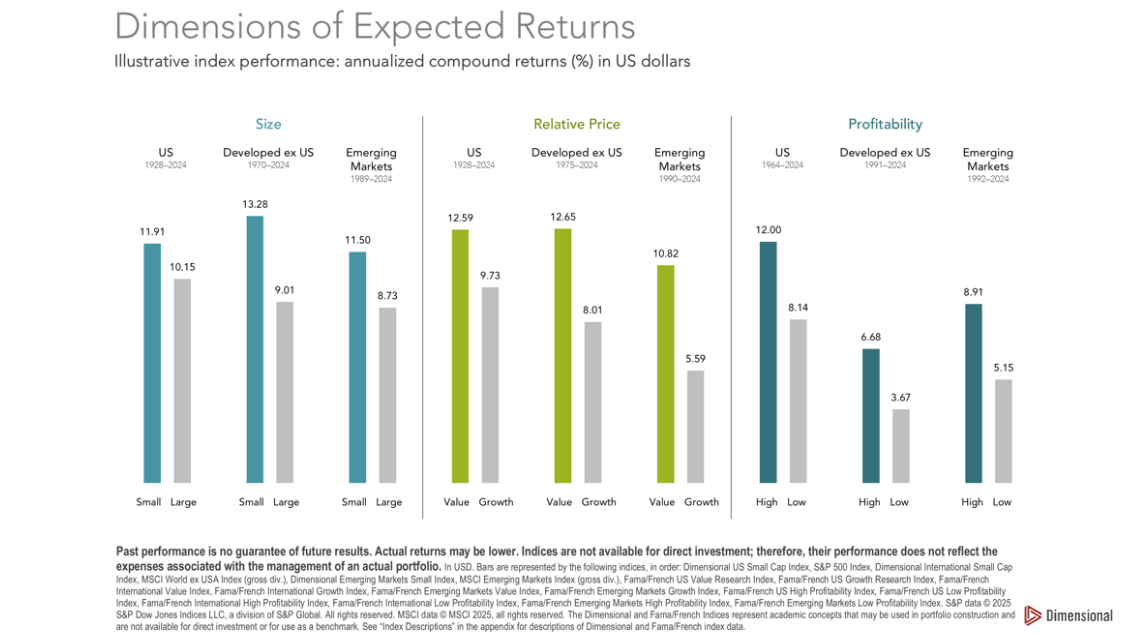

The three most widely supported equity factors are:

Size: Smaller companies have delivered higher long-term returns than larger companies.

Relative Price: Cheaper stocks (relative to fundamentals) have outperformed expensive growth stocks over time.

Profitability: Companies with stronger profits have historically outpaced lower-profit peers.

These patterns have been observed across many decades and multiple regions, suggesting they reflect how markets reward risk and disciplined behavior rather than fleeting anomalies.

Why Market-Cap Weighting Isn’t the Whole Story

Market-cap weighting is elegant and efficient, but it systematically favors yesterday’s winners. When a stock’s price rises, it becomes a larger slice of your index. When a company is unloved and cheap, its weight shrinks. Over full cycles, that can leave investors holding more of what is popular and less of what is potentially rewarding.

Factor tilts counterbalance that tendency. By nudging allocations toward small, cheap, and profitable companies (while keeping the entire portfolio diversified), you add independent “engines” of return without abandoning the simplicity that makes index investing work.

What the Evidence Says

Long-run data show that size, value, and profitability have earned return premiums over broad market benchmarks. Those premiums aren’t guaranteed and they don’t show up every year, but across long horizons they have been persistent and global. Importantly, the edge strengthens as your time horizon lengthens:

Over one-year periods, factor outperformance is modest and variable.

Over 10- and 15-year rolling periods, the odds of factors beating their counterparts improve substantially.

Diversifying across multiple factors further reduces the chance that your portfolio relies on a single source of return.

The message for retirees and long-term investors is simple: patience and diversification are key. No factor wins every year, but the combination of several, held over full market cycles, has historically tilted outcomes in your favor.

Annualized performance of small cap, value, and high profitability stocks compared to their counterparts

Risk and Behavior: Why Factors Persist

Factors earn a premium for two core reasons:

Risk: Small companies are less liquid and more volatile; value stocks can be economically stressed; profitability signals can fluctuate with business cycles. Investors demand compensation for these risks.

Behavior: Value and small-cap investing often feels uncomfortable. Humans extrapolate recent trends and crowd into what’s already worked. Factor investing requires sticking with a disciplined process precisely when it’s emotionally hardest.

That discomfort is the “price” of the premium. The payoff for accepting measured, well-researched risks is what makes factor tilts a compelling enhancement to a plain index approach.

How to Build a Factor-Informed Portfolio

Step 1: Keep the Core Principles

Diversification across thousands of stocks, globally. Low costs. Tax awareness. A written plan. Factors are an enhancement, not a replacement for good habits.

Step 2: Add Targeted Tilts

Introduce small, systematic overweights to size, value, and profitability. This can be done with multi-factor funds or with a mix of single-factor funds. Keep tilts meaningful but moderate so the portfolio still behaves like a diversified market portfolio.

Step 3: Stay Global

Apply factor tilts across U.S., developed international, and emerging markets. Broader opportunity sets increase diversification and reduce reliance on any one country’s market regime.

Step 4: Rebalance with Rules

Set a rebalancing policy by calendar (e.g., annually) or tolerance bands. Rebalancing enforces discipline—trimming what has run up and adding to what is out of favor—without guessing or market timing.

Retirement, Taxes, and Planning: Making Factors Work in the Real World

Integrating factor investing into a retirement plan is about more than choosing funds. Coordinating asset location, withdrawals, and rebalancing can improve after-tax results and cash-flow reliability.

Asset Location

Place tax-inefficient assets in tax-advantaged accounts when possible:

Higher-turnover or small/value-tilted funds may realize more taxable distributions. Favor tax-deferred or Roth accounts for these.

Broad market or tax-managed funds often fit well in taxable accounts, especially those with low dividend yields and good tax-loss harvesting potential.

Withdrawal Sequencing

Thoughtful sequencing can reduce lifetime taxes and keep factor tilts intact:

In lower-income years (often early retirement), realize long-term gains from taxable accounts at favorable rates while performing partial Roth conversions from tax-deferred accounts.

In higher-income years, lean more on cash buffers and previously harvested lots to limit bracket creep.

Coordinate portfolio sales with rebalancing so you raise cash while maintaining your factor exposures.

Tax-Loss Harvesting and Gain Harvesting

Tax-loss harvesting in taxable accounts can offset gains and ordinary income (subject to IRS rules), providing tax flexibility without changing your strategic factor tilts.

Gain harvesting may be attractive in years when your taxable income sits in lower long-term capital gains brackets, allowing you to refresh cost basis with minimal tax impact.

Managing RMDs and Social Security

Required minimum distributions from tax-deferred accounts can be lumpy. Use rebalancing around RMD season to keep exposures aligned.

Monitor how withdrawals affect provisional income and Medicare premium brackets; coordinate sales across accounts to avoid unpleasant surprises.

Behavioral Guardrails

Build a cash and high-quality bond sleeve sized to your spending needs for several years. This reduces pressure to sell equities during downturns, making it easier to stick with factor tilts when they are temporarily out of favor.

A Sample Blueprint (Illustrative Only)

Core global equity allocation anchored by total market funds.

Add multi-factor or dedicated small value and high-profitability sleeves in U.S. and international markets.

Calibrate tilts to your risk tolerance and time horizon; modest tilts can go a long way.

Pair with high-quality bonds for stability and spending needs.

Rebalance annually or when allocations breach tolerance bands.

This maintains the simplicity and broad reach of indexing while introducing additional return drivers.

Common Mistakes to Avoid

Overconcentration in a single factor. Diversify across size, value, and profitability to smooth the ride.

Chasing recent winners. Factors are cyclical; expect stretches of underperformance and prepare for them in advance.

Ignoring taxes. Where you hold factor funds and how you trade them can materially change after-tax returns.

Abandoning the plan in a slump. The edge shows up over long horizons. Changing strategies mid-cycle often locks in underperformance.

Due Diligence on Implementation

There are multiple providers offering rules-based, low-cost funds that target size, value, and profitability. Evaluate:

Methodology: How the fund defines and weights factors, and how it handles rebalancing and trading.

Costs: Expense ratios, spreads, and implementation slippage.

Tax efficiency: Historical distributions and turnover patterns.

Fit: How the fund complements your existing holdings and your rebalancing policy.

Choose consistent, transparent approaches that align with your philosophy and tax situation.

Who Should Consider Factor Investing

Long-horizon investors who can commit to a disciplined, rules-based process.

Retirees seeking multiple independent engines of return to improve the reliability of outcomes over full cycles.

Planners looking to integrate market evidence with smart tax and withdrawal decisions, rather than making concentrated, all-or-nothing bets.

If your priority is a resilient retirement plan—spanning bull markets, bear markets, and everything in between—layering factor tilts onto an index core is a pragmatic, evidence-guided path.

Putting It All Together

Index funds remain a fantastic foundation. Factor investing builds on that foundation by tilting toward characteristics that have historically offered higher expected returns, without sacrificing diversification or discipline. When paired with thoughtful retirement planning—asset location, tax-aware withdrawals, and rules-based rebalancing—you can improve after-tax outcomes and strengthen the reliability of your plan.

The goal isn’t to predict which engine will lead next year. It’s to build a diversified portfolio where several engines can power progress over decades, giving your retirement plan a better chance to meet spending needs with fewer compromises.

Next Steps

Map your current holdings to see where you already have implicit factor exposure.

Decide on modest, durable tilts across size, value, and profitability.

Align asset location and rebalancing rules to your tax profile and spending plan.

Document the strategy so you can stick with it during inevitable dry spells.

If you want a retirement plan that incorporates factor investing in a tax-smart, practical way, consider a personalized review that coordinates investments, taxes, and planning into one integrated strategy.

Share:

About the author

Jake Skelhorn

Jake is a CFP Professional with a focus on planning for both traditional and early retirement. He’s a Florida native, growing up in Fort Lauderdale and now residing in Jacksonville with his husband Chris and their 120-lb “puppy” Barli. Jake enjoys cooking (favorite cuisine to make is Thai), traveling, and spending time with friends and family as much as possible.

.png)