%20(1).png)

Retirement can feel like stepping into the unknown. If you're like Peter—a 54-year-old with a pension, a solid investment portfolio, and a desire to retire early—you're probably wondering: Can I afford to retire now?

In this post, we’ll walk through a real case study of a client I’ve worked with, using a detailed retirement income plan that factors in taxes, spending, investment allocations, and guardrail-based withdrawal strategies. The goal? To give Peter confidence in his retirement planning and help others like him find clarity in their own journey.

Watch on Youtube:

Peter is 54 years old, earning $85,000 per year, and already collecting a $33,000 annual pension from the California Public Employees Retirement System (CalPERS). He's saved approximately $727,000 across various accounts and is on track to hit $800,000 by the time he plans to retire in June 2026.

His goal is to retire early and live off his savings, pension, and eventually Social Security. His baseline spending needs? About $3,000 per month in discretionary expenses (or $46,000 annually), plus taxes and housing-related costs like mortgage payments and insurance.

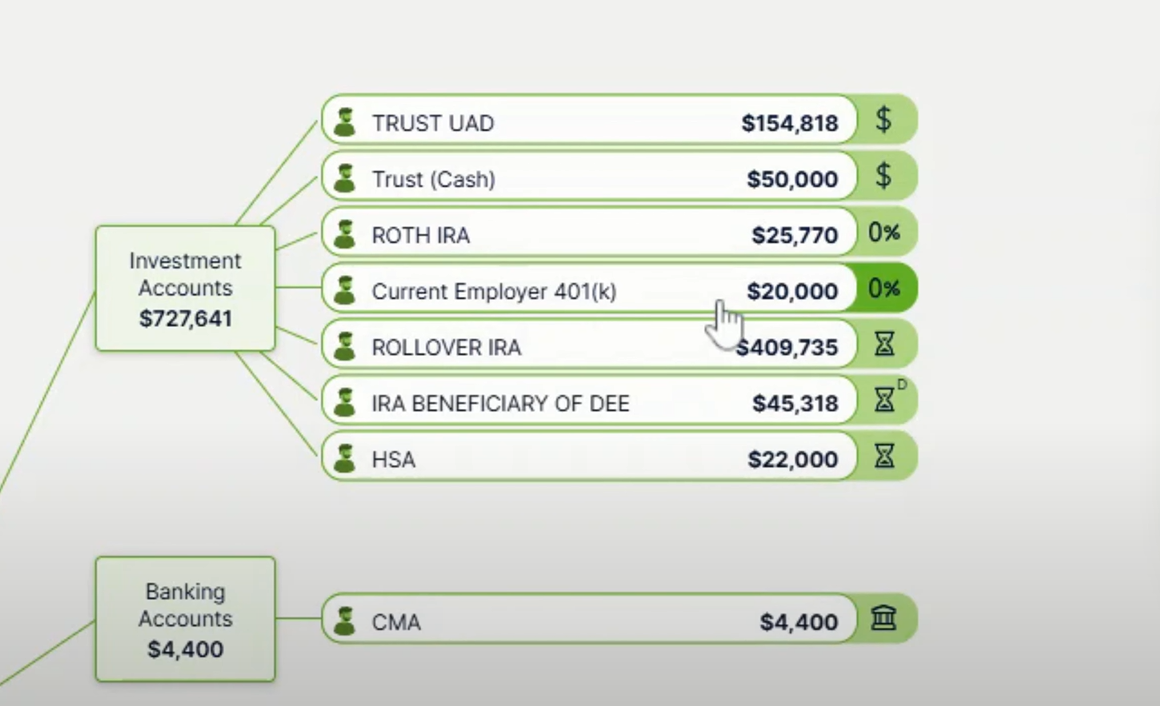

Peter's investment accounts include:

This spread of accounts allows for smart tax planning. Here’s how his assets break down in tax terms:

Why does this matter? Because taxes in retirement are just as important as your total savings. Having funds in each tax category gives Peter the flexibility to strategically withdraw money in ways that lower his tax bill and avoid early withdrawal penalties.

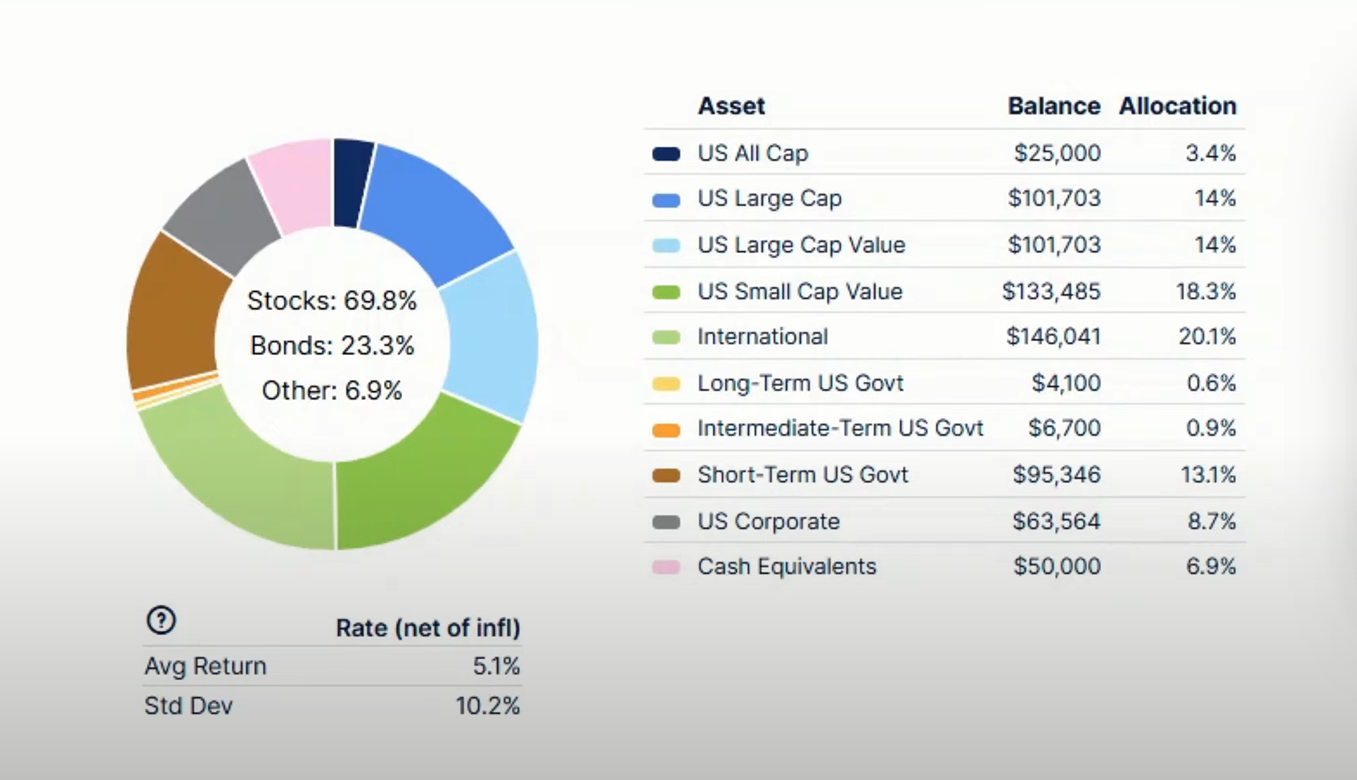

Using a conservative return assumption of 5.1% after inflation, Peter’s portfolio is built with a 70/30 split between stocks and bonds. This allocation offers long-term growth while managing volatility—important for someone entering retirement early.

Because Peter already has a pension acting as an income floor, he felt comfortable taking on some investment risk. The portfolio is well-diversified and built to withstand the ups and downs of retirement spending.

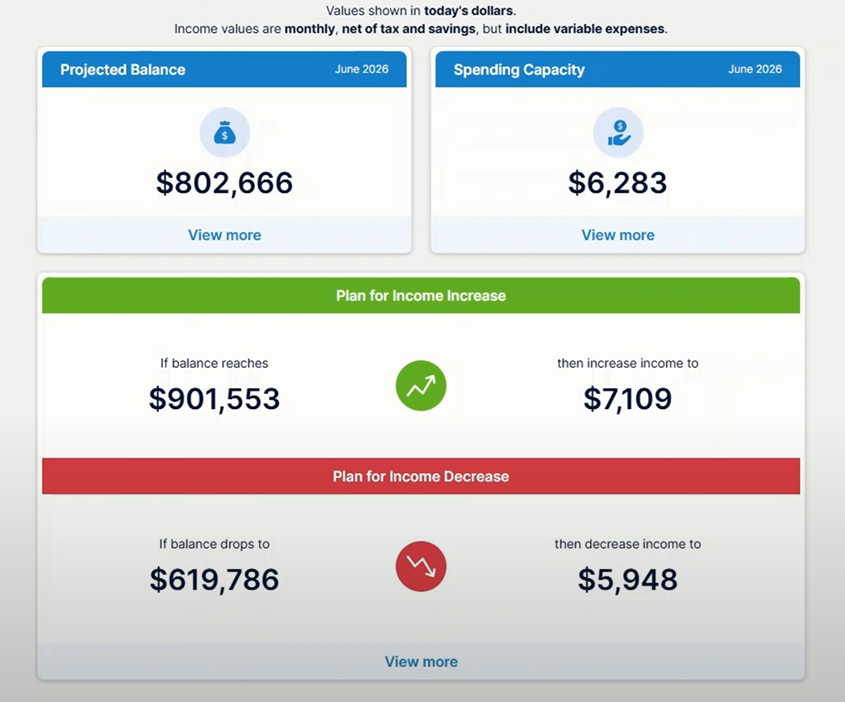

The cornerstone of Peter’s plan is a retirement income guardrail strategy. This strategy determines how much Peter can safely withdraw from his portfolio each month, while adjusting for market fluctuations over time.

Think of guardrails as financial bumpers that help you adjust spending based on how the market performs.

Using this method, Peter can safely start retirement by spending about $6,300 per month (after taxes). This number includes:

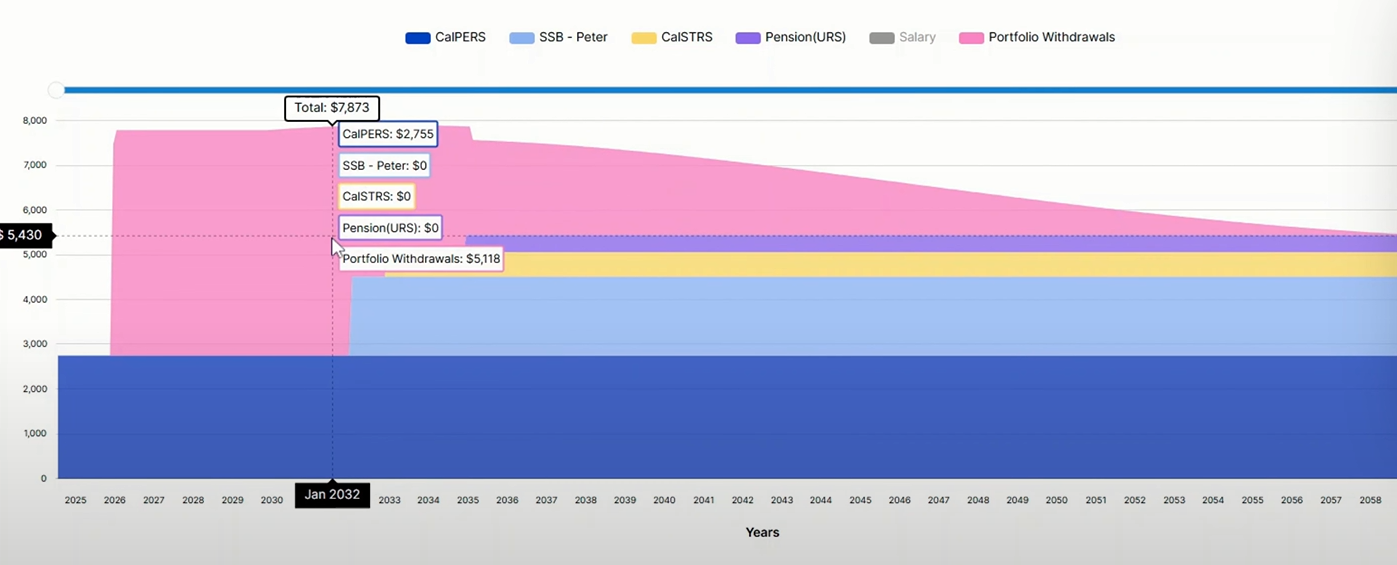

In the early years of retirement, Peter will withdraw around $5,000/month from his investment accounts. That’s about a 7% withdrawal rate—which sounds high if you’re comparing it to the old-school 4% rule. But here’s the nuance:

This dynamic spending strategy helps Peter enjoy more in the early years when he’s healthy and active, without jeopardizing long-term stability.

Peter plans to retire before turning 65, meaning he’ll need health insurance through the marketplace for several years. Because his income in retirement will be low—thanks to strategic withdrawals—he qualifies for tax credits that significantly lower his premiums.

This helps bridge the gap until he becomes eligible for Medicare at 65, reducing the risk of unplanned healthcare expenses in early retirement.

Even the best retirement plans should account for worst-case scenarios. That’s why we use stress testing to simulate how Peter’s plan would have performed during previous market downturns like:

By using historical data, we can see that:

This approach reassures clients that even in a crisis, a well-designed plan with flexible adjustments can weather the storm.

Peter's diverse tax buckets play a critical role in minimizing retirement taxes. Here's how we approach it:

This withdrawal order helps keep Peter in a lower tax bracket, reduces future RMD burdens, and preserves flexibility.

Peter’s case study is a blueprint for retiring with confidence—even before 60. The keys to his success:

Everyone’s situation is unique, but the principles behind Peter’s plan—diversification, tax efficiency, adaptive spending, and contingency planning—can apply broadly.

If you’re wondering how your own savings, pension, or Social Security might translate into a reliable monthly income, I offer a free retirement income assessment for anyone considering working with our firm.

👉 Schedule Your Free Retirement Income Assessment