.png)

If you’re nearing retirement or have already crossed that milestone, and you’ve managed to save $1 million or more in your 401(k), IRA, or brokerage accounts, congratulations — you’ve done a great job. But if you're still wondering, “Is this enough?”, you’re not alone.

Many retirees face uncertainty not from a lack of savings, but from not having a strong retirement income plan. The good news is that there’s a modern strategy you likely haven’t heard from traditional financial advisors — one that encourages smarter spending without jeopardizing your long-term security.

Watch on YouTube:

Jake Skelhorn, Certified Financial Planner and co-founder of Spark Wealth Advisors, observed a common trend during his tenure at a large wealth management firm: new retirees tend to spend too little, not too much. Fear of running out of money causes people to overly restrict their lifestyle — even when they could afford more.

This overly conservative approach often stems from outdated income rules and tools that large firms stick to — not necessarily because they’re the best for clients, but because they help maximize assets under management, which increases fees.

Let’s walk through the key pitfalls in traditional retirement planning and explore a better, more flexible strategy.

The 4% rule is one of the most well-known retirement withdrawal strategies. It suggests that you can withdraw 4% of your starting portfolio balance in your first year of retirement, and then adjust that number annually for inflation.

For example, if you retire with $1 million, you'd withdraw $40,000 in your first year and increase it slightly each year.

But here’s what’s wrong with this approach:

The 4% rule is based solely on your starting balance. If your investments perform well, you might have a significantly higher portfolio in a few years — but your income doesn’t adjust accordingly. This results in underspending and lost lifestyle opportunities.

In reality, retirees spend more in their early, active years and gradually less as they age. Research from JPMorgan Chase confirms that retirement spending declines over time, even accounting for inflation. The 4% rule doesn’t reflect this natural spending curve.

The 4% rule was designed to survive the worst 30-year market periods in history. But what if your retirement lands during average or even strong market years? Studies show you could potentially withdraw 5–10% annually and still be fine. That’s potentially $60,000 more per year in income than the 4% rule would suggest.

Monte Carlo simulations are often used in retirement planning to test thousands of possible future scenarios based on market returns, inflation, and life expectancy. The result is a “probability of success” score — the chance that your money will last until the end of your life.

But this method has some serious limitations:

These gaps can leave retirees anxious, leading to bad investment decisions (like panic selling) or unnecessary lifestyle restrictions.

Retirement income guardrails are a dynamic and flexible spending strategy designed to adjust based on actual portfolio performance — not theoretical averages.

This approach gives retirees confidence to spend more while also having a plan in place if the market underperforms. You start with a safe spending rate (often more than 4%) and adjust over time based on upper and lower thresholds.

Let’s break it down:

Imagine your portfolio is $1 million, and based on your personal inputs, your guardrail strategy says you can safely withdraw $60,000 per year.

If your portfolio grows significantly (say to $1.3 million), you’ll cross the upper guardrail, which tells you it’s safe to increase your spending — perhaps an extra $1,500/month.

If your portfolio drops (say to $800,000), the lower guardrail kicks in, signaling it’s time to reduce spending slightly — maybe by $350/month — to avoid drawing down too quickly.

This system adapts to reality in real-time, allowing you to make intelligent, small adjustments rather than overreacting.

Jake shares the story of clients David and Brad, both 65, with $1.6 million saved across IRA, Roth IRA, and taxable accounts.

If their portfolio increases to $2 million, they could boost monthly income by $1,500.

If the market dips, they may need to reduce spending by as little as $350/month.

This dynamic plan gives David and Brad the flexibility to enjoy their active years more fully while still protecting against worst-case outcomes.

Another enhancement is using an age-based spending path, which adjusts withdrawals to reflect realistic behavior — increasing each year by inflation minus 1%.

This assumes you’ll spend more in the early years when travel and hobbies are a priority and less later on when health or mobility might reduce expenses.

It’s a smart planning tactic that maximizes joy early in retirement — when it matters most.

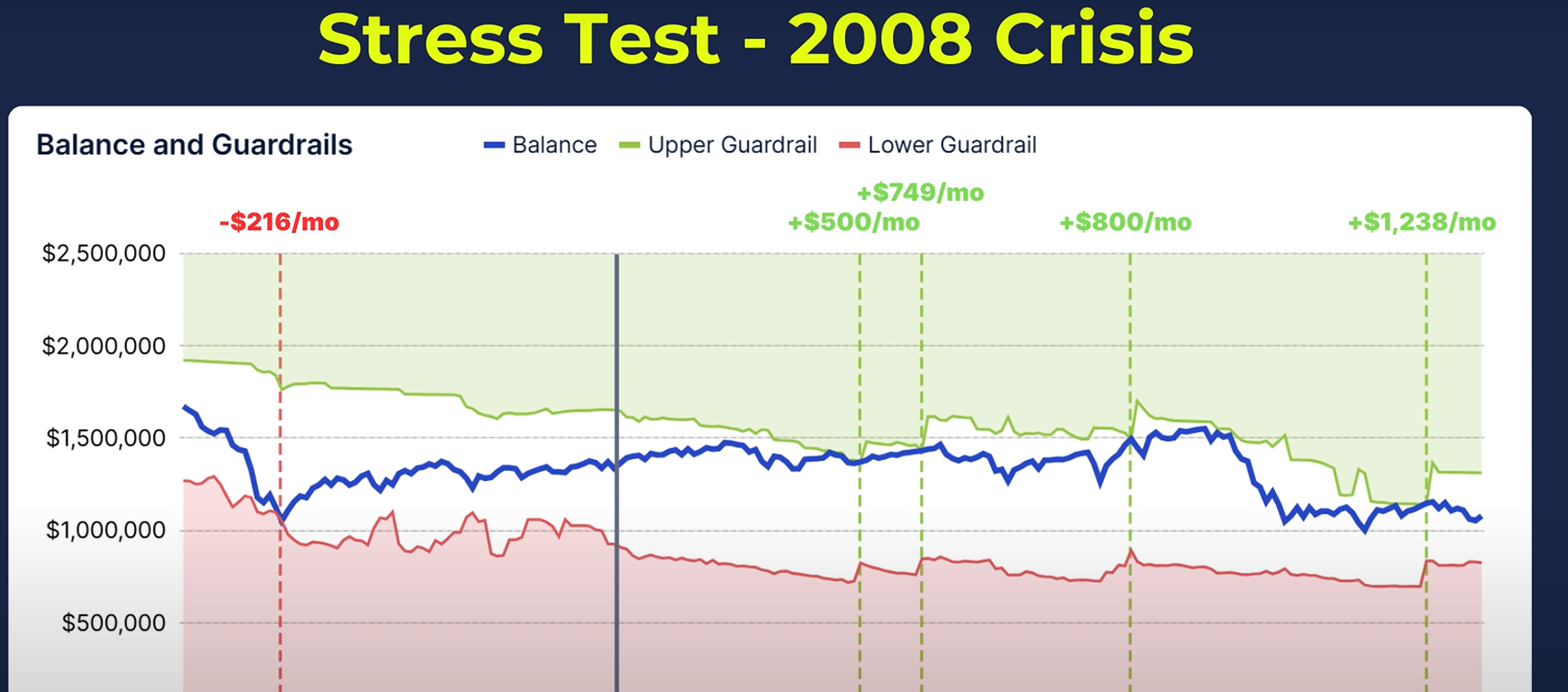

Jake also stress-tests plans like David and Brad’s against past crises like the 2008 recession.

If they had retired right before the crash, their portfolio would have triggered the lower guardrail, leading to a temporary $216/month spending reduction.

But after recovery, they would hit the upper guardrail multiple times — eventually increasing their spending above the original withdrawal level.

This approach turns volatility into actionable insight, rather than fear.

One of the most empowering messages in this strategy is that you don’t need annuities, life insurance policies, or private equity to have peace of mind.

You just need:

Speaking of taxes — they’re a critical part of any retirement planning conversation.

With guardrails, you can also optimize which accounts to draw from and when (e.g., taxable, Roth, traditional IRA) to reduce your long-term tax burden.

You might start withdrawals from taxable accounts early to delay Social Security and reduce required minimum distributions (RMDs) later. You might also take advantage of low-income years to do Roth conversions at favorable tax rates.

A good retirement plan is a tax-efficient plan — and guardrails make that coordination easier.

If you're intrigued by this approach and want to see how it could apply to your situation, Jake and his team at Spark Wealth Advisors offer a free guardrails assessment.

This includes:

They’re a fee-only fiduciary firm, meaning no commissions, no insurance product sales, and no hidden agendas — just advice in your best interest.

Final Thoughts

You’ve saved diligently — now it’s time to spend confidently. The traditional rules may be holding you back from living your best retirement. By embracing smarter planning tools like retirement income guardrails, you can enjoy more of what matters, with less fear of running out of money.

If you’re still working, you may not need as much as you think to retire comfortably. If you’re already retired, you might be able to spend more than you think.

Retirement, taxes, and planning don’t need to be rigid or overwhelming — not when there’s a better strategy built just for you.