Inheriting an IRA isn’t as simple as cashing in and walking away. With recent updates to federal law—including the SECURE Act of 2019 and SECURE 2.0 of 2022—the rules governing inherited IRAs have changed dramatically.

If you're not careful, you could end up with an unnecessarily large tax bill, or worse, face penalties from the IRS. In this guide, we’ll cover eight often-overlooked rules that can help you navigate inherited IRAs more strategically, all while maximizing your retirement income and minimizing taxes.

Watch on YouTube:

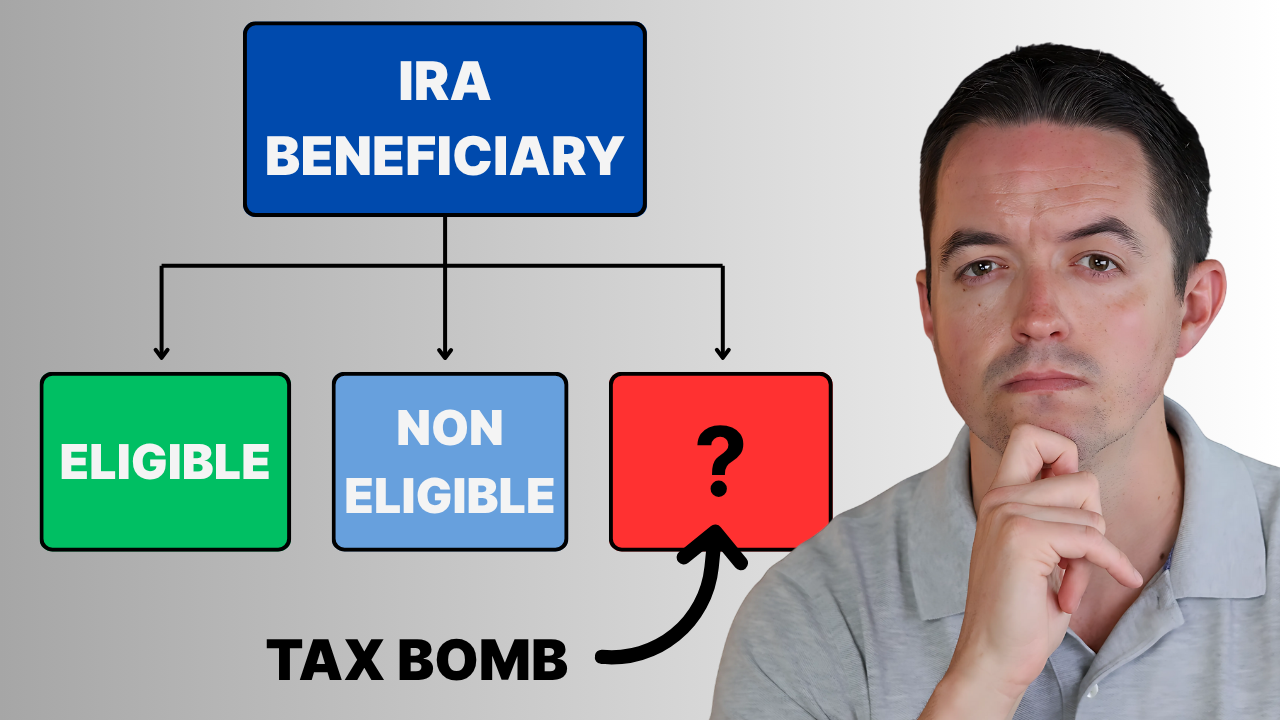

Before diving into the rules, it’s crucial to understand your beneficiary classification. The IRS places beneficiaries into three main categories:

Your classification determines how long you have to distribute the IRA and what tax planning strategies are available.

Most people assume they have 10 years to empty an inherited IRA. However, if you inherit through a non-designated beneficiary—such as through a will or non-see-through trust—you could fall under the 5-year rule.

That means you must withdraw all funds by December 31 of the fifth year after the original account holder’s death. For example, if someone dies in 2025, you must fully distribute the account by the end of 2030—not 2035.

This can lead to a condensed withdrawal schedule, triggering significant income taxes in a short period and potentially pushing you into a higher tax bracket.

If you and siblings inherit an IRA together and don’t split it into separate inherited accounts by September 30th of the year after the original owner's death, the required minimum distributions (RMDs) could be based on the oldest beneficiary’s age.

For example, if you're 45 and your sister is 65, your RMDs will be calculated using her life expectancy, not yours. That translates to larger distributions and more taxable income.

The solution? Split the inherited IRA into separate accounts before December 31st of the year after the death to use your own RMD schedule.

A common mistake in retirement planning is thinking you can offset inherited IRA RMDs by taking more from your own IRA. Unfortunately, that’s not allowed.

RMDs for inherited IRAs must be taken separately, even if you have multiple inherited IRAs. The only exception is if they share the same deceased owner, same beneficiary structure, and same timeline. Otherwise, you must track and withdraw each account independently.

Another widespread myth is that you can convert an inherited IRA to a Roth IRA. For most non-spouse beneficiaries, this is not permitted.

Only spouses who elect to treat the IRA as their own may have this option, and even then, the account must not already be a "twice-inherited" IRA. If you're a child or grandchild, your only option is to withdraw and pay ordinary income tax—no conversions allowed.

If a minor child inherits an IRA, they are eligible for a “stretch” provision, meaning they can take RMDs instead of being subject to the 10-year rule. But this benefit only lasts until they reach the age of majority—typically 18 or 21 depending on the state.

Once they hit adulthood, the 10-year rule kicks in immediately. So, a 10-year-old might have 8–11 years using RMDs, then 10 more years to fully distribute the account. This creates a unique retirement planning opportunity for families to coordinate withdrawals over time.

If you began taking inherited IRA RMDs before 2022, the IRS now uses new life expectancy tables introduced in 2022.

That means your current withdrawal amount might be incorrect if you’re still referencing outdated calculations. It’s a technical update, but a critical one—incorrect withdrawals can result in IRS penalties. Always refer to the latest tables available on IRS.gov.

Here’s a rare gem: if the deceased person's estate was large enough to pay federal estate tax, you might qualify for an Income in Respect of a Decedent (IRD) deduction.

This little-known deduction lets you offset income taxes on IRA withdrawals by deducting a portion of the estate tax already paid on that IRA.

While it's not common (thanks to the high estate tax threshold), if it applies, it can significantly reduce your tax bill. Make sure to keep detailed records and consult a tax professional familiar with IRD rules.

If the inherited IRA holds an annuity, things get even more complex. Annuities have built-in withdrawal schedules and penalties, which may not align with the IRS’s required distribution timelines.

For example, the annuity might offer guaranteed withdrawals over 15 years, but the IRS could require full distribution in 5 or 10 years, depending on your beneficiary status. Always coordinate with the insurance company to align both sets of rules, or risk triggering penalties or surrender charges.

Inheriting an IRA can be a financial blessing—but it’s also a tax and planning minefield if you're not careful. Understanding these eight overlooked rules is key to managing withdrawals, minimizing taxes, and aligning inherited assets with your own retirement plan.

If you’ve recently inherited an IRA—or expect to—it's wise to consult with a Certified Financial Planner (CFP) or tax advisor to develop a strategy tailored to your situation.

Because with the right planning, what you inherit can work for your future retirement, not against it.

Spark Wealth Advisors offers personalized planning to help you manage inherited assets wisely. If you’d like to see how your inherited IRA fits into your broader financial goals, reach out for a consultation.

Download the free Inherited IRA Guide here